|

Getting your Trinity Audio player ready...

|

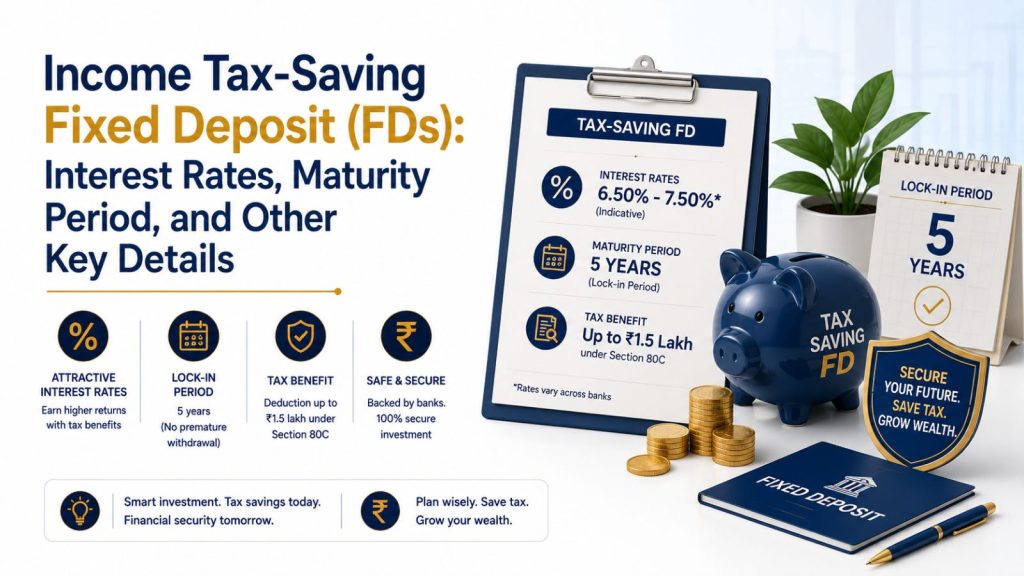

Tax-Saving Fixed Deposits (FDs) remain a very favorable choice of investments for those who wish to enjoy tax benefits along with stable yields. Tax-saving FDs eligible for tax deductions fall under Section 80C of the Income Tax Act, 1961, provided that the total cap is not exceeded as per the provisions of the Act and that the investor chooses the old tax regime. From 6th July 2026 onwards, there are various options available for tax-saving FDs issued by banks at varying rates of interest.

What Is a Tax-Saving Fixed Deposit?

Tax Saving Fixed Deposit is one particular type of FD scheme offered by banks, which requires a compulsory lock-in period of five years from the date of opening of the deposit account, during which the deposit account cannot be withdrawn prematurely or pledged as collateral.

These FD schemes are meant to offer an opportunity to the eligible taxpayers to avail themselves of deductions under section 80C, but the income received from the deposit is taxable under the respective income tax slab.

Invest in bonds & earn 9-14%* p.a fixed returns

Start investing with just 10K & grow your wealth with fixed-return bond opportunities.

Explore NowLatest Interest Rates

Tax-saving FD rates vary with each bank and keep changing from time to time. For the year 2026, tax-saving FD rates are offered by most public and private banks at a range of 6.25% – 7.10% per annum for regular citizens. In case of senior citizens, the banks may provide some added interest benefits according to their policies.

Small Finance Banks

Small finance banks and NBFCs consistently offer the highest FD slab rates.

- Suryoday Small Finance Bank: Up to 8.10% p.a. (30 months).

- Utkarsh Small Finance Bank: Up to 8.10% p.a.

- Jana Small Finance Bank: Up to 8.00% p.a.

Large Private Sector Banks

Rates are quite competitive, especially for longer terms.

- HDFC Bank: Offers 6.25% (1-year) to 6.50% (15-months to 5-years).

- ICICI Bank: Offers 6.25% (1 year) up to 6.50% (up to 5 years).

- IDFC FIRST Bank: Up to 7.35% p.a. (3-year).

- YES Bank: Up to 7.25% p.a.

Public Sector Banks (PSUs)

Public banks generally offer more conservative, stable returns.

- State Bank of India (SBI): 6.25% (1-year) to 6.45% (Highest slab/special tenures).

- Bank of India: Up to 6.85% p.a.

- Indian Bank: Up to 6.80% p.a.

Post Office Small Savings

- 1-Year: 6.90% p.a. | 2-Year: 7.00% p.a. | 3-Year: 7.10% p.a. | 5-Year: 7.50% p.a. [1]

Note: Interest rates are subject to frequent changes based on RBI repo rates and bank policies. Senior citizens typically get 0.50% to 0.80% extra.

Investors should refer to the latest rates being offered by the concerned bank, as they are regularly updated.

Latest Fixed Deposit Rates:

- Income Tax-Saving Fixed Deposit (FDs): Interest Rates, Maturity Period, and Other Key Details

- SBI FD Interest Rates 2026: Latest Rates, Features, and Things Investors Should Know

- Premature Withdrawal Rules for Bank FDs: Penalties Explained

Maturity Period & Lock-In Period

The lock-in period of 5 years for a tax-saving fixed deposit is one of its key distinguishing factors.

Key points to note are the following:

- Minimum period of investment: 5 years (Compulsory)

- There can be no premature withdrawal.

- There can be no loans against tax-saving FD.

- Interest is calculated based on what was opted for at the time of making the deposit.

As the investment period will remain locked in for 5 years, investors need to evaluate their liquidity requirements before investing.

Tax Benefits and Taxation

FDs that save taxes fall under Section 80C of the Income-tax Act and are eligible for deductions subject to the maximum amount specified under the act. However, this is possible only for those taxpayers who opt for the old tax regime.

Other things worth mentioning are:

- The earnings are taxed according to the tax slab of the investor.

- Banks may deduct TDS on the interest payable if the income exceeds the threshold set by the Income-tax Act.

- Investors need to declare the income from interest on their ITR.

Who Can Invest in a Tax-Saving FD?

A tax-saving FD may be ideal for people who:

- Are eligible for Section 80C deduction under the old tax regime.

- Are you looking for a fixed-income investment with a definite tenure?

- Do not need their investment funds for five years.

- Are you ready to be taxed on the interest income?

As always with any other investment decision, one should make sure that the investment suits their needs.

Key Takeaway

Income tax saving FDs continue to be a popular income tax-saving tool for those eligible taxpayers who fall under the old tax structure. Though income tax saving FDs provide tax benefits through Section 80C and a fixed rate of interest over five years, it is important to note that interest from these deposits is taxable, and the funds cannot be withdrawn before the end of the period. The comparison of interest rates and other conditions will enable the investors to make an informed decision.

Ready to Invest?

Visit GoldenPi to explore current bond options. Compare yields, ratings, and tenures in one place and invest online with as little as ₹10,000.

Disclaimer:

Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities and municipal debt securities/securitized debt instruments are subject to credit risks, market risks, and default risks, including delay and/or default in payment. Read all the offer-related documents carefully. This blog/article should not be construed as financial advice or as an offer or recommendation to buy or sell any security or any products/services of/on GoldenPi or any product/services of its third-party client(s). For a detailed calculation of YTM, visit our website. T&C’s Apply.